Digital Finance

Capability Statement

Banking the World |

|---|

|

"Digital channels can drastically drive down costs for customers and service providers, opening the door to remote and underserved populations. Financials regulators around the world have realized the tremendous role DFS can play for financial inclusion and seek to unlock this potential by creating enabling environments for digital financial services." AFI |

Going Digital: The Future is Now!

The digital revolution has taken many organisations by surprise. If you want to serve your staff / clients / customers and prosper in an increasingly competitive market, then you must take advantage of the opportunities DFS offers. Since 2012, LFS has been at the forefront of promoting DFS for financial inclusion, as with the right market assessment, strategy, design and implementation, digital channels and products can help organisations tap into new markets, increase client loyalty, reduce transaction costs, increase transparency and speed up reporting.

If FIs want to serve their clients well and survive in this increasingly competitive market, they must take advantage of the opportunities digital finance offers. They must introduce products and services that are tailored to the specific needs of the underserved population. As such, FIs have been rolling out agent and mobile banking. Agribusinesses are looking for more efficient ways to pay their smallholder farmers (than cash). There is scaling up of mobile money by Mobile Network Operators and Payment Service Providers. Policy makers and regulators are making enabling conducive environments. However, Financial Institutions (FIs) face growing competition from Telcos, Fintechs, Big Techs (Alibaba, Google, Apple, Facebook and Amazon) and an influx of innovative, flexible, and customer-oriented products and services.

LFS believes that through partnership development, knowledge and experience, and technical know-how we can help clients with their digital transformation journey. For example, innovative solutions are now looking beyond savings and loan products and are incorporating advanced products such as pay-day loans, bill payments and insurance. With this in mind, it’s imperative to design customer centric products and services that address the necessities and desires of the unbanked, focusing especially on the unique needs of women.

LFS:

- Helps our clients put their customers first

- Believes in Human Centred Design / customer centricity

- Employs product prototyping to get quick feedback

- Always considers consumer protection issues

- Follows project and change management best practices

Digitization: is changing from analog to digital i.e. it’s the information you’re digitizing. For example, replacing pen and paper registration with a Digital Field App / tablet.

Digitalization: is the process of employing digital technologies and information to transform business processes and operations. An example is changing from manual data entry into the Core Banking System (CBS) to a DFA that automatically updates the CBS.

Digital Transformation: is not limited to digital projects but a broader term revolving around being customer rather than transaction-driven. It requires cross-cutting departmental change. Initiatives will typically include several digitization and digitalization projects, underpinned by a digital transformation strategy. This strategy should be aligned to the global business plan.

As a specialist advisory firm, LFS supports clients to make the right decisions and realise their digital opportunities. We have implemented DFS projects for a variety of clients and gained profound knowledge of digital finance solutions and a strong expertise in defining new business models. LFS combines the business and technology expertise to support a range of organisations with a broad spectrum of services to scale up and manage risks for lasting success. By leveraging DFS, LFS can help you to reduce your operational costs, increase your outreach, and develop / modify products or services which are more customer centric. For instance, in the microfinance sector LFS has helped clients with strategizing and implementing agent banking and mobile money solutions to customers who were previously excluded.

For the last 20 years, LFS has built up a distinctive and exceptional track record in the financial inclusion sphere and which has included market assessments (macro level), feasibility studies (micro level) and a range of Digital Financial Services projects.

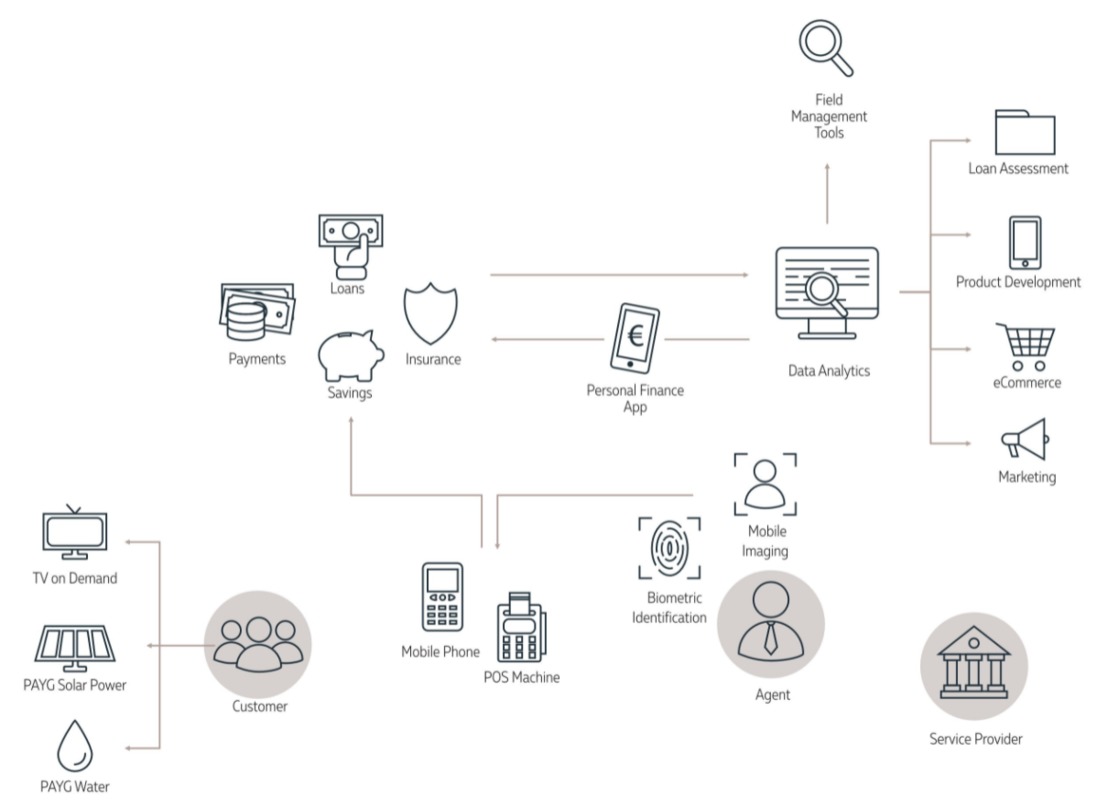

LFS understands that DFS is more than just mobile money, it’s even more than access to financial services (loans, savings, transfers and insurance) but rather it is part of a transformation strategy to make your organisation more customer centric.

Range of Services

Assessments/Research

Market Assessments

Analyse the full ecosystem of stakeholders: regulators, service providers, business drivers etc.

Market Demand Analysis

Demand assessment for DF services across various segments, including analysing the receptiveness of clients to potential channels of delivery.

Market Supply Analysis

Assessment of the supply of DF service among competitors, specifically in the bank’s target market area.

Feasibility Studies

Elaborating the existence of aggregators, role of mobile network providers, IT interfaces and software integration.

Strategy

Strategy Formulation and Execution

Support executive leadership to identify, articulate and execute on digital opportunities that will increase competitive advantage.

Cost/Benefit Assessment

Evaluating the delivery channel options from the point of view of the bank in terms of return on investment as well as the larger strategic implications.

Business Plan

Roadmap of attainable business goals and how to achieve them that includes business concept, market strategy and the financial plan.

Implementation

Product Design (using HCD)

Including pricing and costing mechanism as well as recommended delivery channels.

Channel Development

Setup and manage agent networks that provide the physical backbone of mobile money (cash in - cash out points).

Service Development

Whether digital loans, loyalty programs, enabling customers to deposit onto their accounts, pay bills, internal bank transfers, balance inquiry and mini statement.

Training

Capacity building of all relevant staff through classroom and on the job trainings.

Policies, Processes and Procedures

Map and improve internal workflows using Bizagi Project Management Tool (BPMN) 2.0

Tools

Field Data App

Including pricing and costing mechanism as well as recommended delivery channels.

DFS Readiness/Gap Analysis Tool

A tool that helps identify where you should make new investments and capabilities to fully leverage the possibilities and opportunities that new technologies offer while ensuring flexibility and adaptability for future innovation. The resulting report provides a benchmark against other financial institutions in your country, region or network. This exercise builds the foundation for a digital transformation strategy and roadmap that is aligned to the global business plan.

Business Optimisation Tool(BOT)

Using BPMN 2.0 to map and improve process, LFS exports the data and uses it in the BOT to measure the financial impact (cost savings and new revenue) of the new processes and procedures.

Project Spotlights

Developing the Payments Strategy for Vodafone Fiji M-Pesa

In 2019, UNCDF contracted LFS to provide technical assistance for the development of Vodafone Fiji’s digital payments strategy. Vodafone is the leading operator of mobile money and m-commerce in the Pacific and wishes to reinforce this market position by aligning its current payment offering and adding further digital financial services and products to the existing ecosystem. Starting with an analysis of the external environment for digital payments and financial services in Fiji and the region, LFS subsequently conducted a diagnostic mission to the Vodafone Headquarter in Suva, Fiji to map existing digital payment services and ongoing payment initiatives and assess the internal digital readiness of all departments. The on the ground mission culminated in a participatory digital strategy workshop with Vodafone’s key executives, during which the key pillars of the digital strategy were agreed and subsequently translated into an aligned and comprehensive strategy document.

Digital Transformation gap analysis (multiple clients and countries)

FIs face growing competition from Telcos, Fintechs, Big Techs (Alibaba, Google, Apple, Facebook and Amazon) and an influx of innovative, flexible and customer-oriented products and services into the financial space. If FIs want to serve their clients well and survive in this increasingly competitive market, they must take advantage of the opportunities digital transformation offers to improve the customer experience and make middle and back office processes more efficient.

Launched in 2020 the digital transformation gap analysis tool has been deployed with 14 clients in 8 countries and giving management, BOD and investors quantifiable data to benchmark and qualitative data to fully understand the FIs position on their transformation journey.

Developing a Digital Field App for Social Fund for Development (SFD)

From 2017 till 2019, LFS worked with the Social Fund for Development (SFD), the Yemenite apex body, to enhance the agricultural loan process via the introduction of a digital tool to improve the collection and analysis of loan data. For this project, a tablet based smart application was developed which allows agricultural loan officers to enter loan data (pictures, GPS locations, financial details and cross-checks) in the field. After data entry, the application can be connected to the MFIs’ back-end systems for information processing. LFS supported two MFIs to successfully pilot and rollout of the smart application. A first benchmarking exercise three months after introduction of the tool revealed that the MFIs were able to increase the average number of monthly loan applications by nearly 20% and reduce backend data entry time from 25 minutes to 10 minutes per application. The app was subsequently introduced by other Yemeni MFIs with the support of SFD.

Supporting AccessBank Tanzania through their Digitization Journey

Under the management and technical assistance of LFS, AccessBank Tanzania (ABT) has engaged on an ambitious digitization journey since 2012 when the bank won a large grant from the MasterCard Foundation.

Following the success of its alternative channels strategy the bank introduced a digital bundle in May 2015, and which included: free current account with free mobile banking transactions (all incoming and outgoing transfers). This was an immediate success and the bank opened more than 30,000 accounts and mobilized more than USD 3 million deposits in under a year.

The digitization agenda is core to the strategy and the bank is currently adjusting its business and operating models to offer a full range of digital services. In 2020, LFS supported ABT in developing an all-digital merchant loan product. Building on M-Pesa’s merchant payment platform - Lipa kwa Simu, and in partnership with Vodacom Tanzania, Vodafone Global and FICO, the project’s objective is to design a credit score based on merchant till & Know Your Business (KYB) in order to provide access to fair-priced funds to merchants.

Digitalising SACCOS payments in Tanzania

In 2020 the Co-operative Development Foundation (CDF) of Canada commissioned LFS to support SACCOSs in Tanzania, Ethiopia and Malawi in digitalising their service offering and thereby enhance enrolment of unbanked rural communities. In Tanzania the assignment was conducted in partnership with SCCULT, an apex organization for SACCOS across Tanzania.

In the project LFS worked on two levels:

- Assessing the market and identifying suitable digital solutions for SACCOS and

- Supporting SACCOS to implement to identified solutions.

The LFS market assessment revealed that less than 5% of Tanzanian SACCOS’ are currently offering financial services through mobile wallets while a majority of members would like to see their SACCOS offering loan repayments and savings deposits via a mobile wallet.

Based on these findings, LFS selected the M-PESA collection and disbursement account for mobile money solution and supported designated SACCOS to implement the same. By the end of the project, LFS had supported three SACCOSs to successfully on-board on the M-PESA payment system, allowing SACCOS member to repay their loans and deposit saving from the convenience of their fingertips.

Project References

Country

Client

Year

Project & Description

Zimbabwe

FINASTRA

2021

Market entry assessment for a shared core-banking and payments solution.

Malawi

FINCA

2021

Digital Transformation support with specific focus on agent commerciliasation, adding VAS products / services and implementation of nano credit savings and loans.

Zambia

AB Bank Zambia

2021

Analysis of rural customer needs including savings groups, farmers and women and definition of digital products on AB Bank’s eTumba wallet which meet rural customer’s need and business opportunities using a human centered approach.

Rwanda

AFR

2021

FINSCOPE DFS Thematic report. Analyse FinScope 2020 dataset and produce a report, prepare a presentation for AFR and its stakeholders and a focus note with infographics for wider publication.

Fiji, Papua New Guinea, Samoa, Vanuatu and the Solomon Islands

UNCDF

2020/21

Diagnostics for eCommerce Payments Aggregation Services in the Pacific Region and identification of opportunities to pool transactions from multiple Pacific markets through payments aggregation services.

Somalia

IFC

2020/21

Market analysis of the financial sector with a focus on Digital Financial Services, Agri-Finance and MSME Finance. Including recommendations for IFC investments.

Afghanistan, Brazil, Ethiopia, Georgia, Malawi, Tanzania, Yemen

Various

2020

Digital Transformation Readiness Analysis for various financial institutions (Commercial Banks, Investment Banks, Microfinance Banks and SACCOs).

Tanzania

AccessBank Tanzania

2020

Design a credit score for digital merchant loans that builds on M-Pesa’s merchant payment platform - Lipa kwa Simu. The project was conducted in partnership with Vodacom Tanzania, Vodafone Global and FICO.

Ethiopia, Malawi, Tanzania

CDF Canada, ILCUF Ethiopia, SCCULT Tanzania, MUSCCO, Malawi

2020

A consultancy for assessing ways that enhance enrolment of the unbanked rural communities to the services and products of ILCUF (Ethiopia), SCCULT (Tanzania) and MUSCCO (Malawi) and support selected SACCOSs to introduce digital financial services (mobile money payment and agent banking services).

Ethiopia

ILCUF

2020

Technical input into mobile money SACCOs pilot report.

Chad

IFC

2019 - 2020

Market analysis of the financial sector with a focus on Digital Financial Services. Including recommendations for IFC investments.

Yemen

KfW

2020

Financial sector development needs assessment and DFS gap assessment.

Chris Statham

Business Line Manager, Digital Finance

For the last 12 years, Chris worked in Sub-Sahara Africa and the MENA region, mostly as a freelance consultant across multiple sectors – finance, agriculture, public health and FMCG, on projects ranging from strategy and business analyst to implementation, partnerships and product development. His previous range of clients included a Payment Service Provider, a Mobile Network Operator (MNO) and a USAID access to finance project in Jordan. Prior to starting his career in development consultancy, Chris gathered 6 years of commercial experience in- UK and Ireland, recently he was the first graduate to become a Certified Digital Finance Practitioner, this complimenting his post-degree certificate in microfinance and degree in Marketing.